|

Home | Search | Browse | About IPO | Staff | Links |

|

Home | Search | Browse | About IPO | Staff | Links |

Unemployment insurance reform: the long road to solvency WHEN THE men in business, labor and government announced at a Statehouse news conference March 17 that they had "solved" the state's unemployment insurance (UI) problem, they spent as much time slapping each other on the back as they did spelling out the terms of the settlement they had reached. For once, reporters could forgive the indulgence. These men had negotiated a three-year agreement representing a $2 billion reform in state UI laws. Under the agreement, the taxes employers pay will rise a total of $1,220 billion and the benefits former employers draw will fall a total of $780 million between April 1983 and July 1986. (Eight days later the General Assembly, as expected, would rubberstamp the "solution" to the state's UI problem. The Senate would amend the negotiated agreement onto H.B. 327, a vehicle readied a month earlier. The Senate would pass it 51-0, the House would concur 107-1, and the governor would sign it into law (P.A. 83-001) March 25.) Aside from the terms, perhaps the most important provision in the agreement is the one which "sunsets" the terms: They are binding until July 1, 1986, when taxes and benefits will revert to pre-reform levels. At the news conference it was Gov. James R. Thompson who started all the backslapping. He said, ". . .there really ought not to be any problem now confronting the State of Illinois, in terms of business economic development. . . that this group couldn't tackle. I for one would like to see this group hang together and start tackling the positive problems — now that they've demonstrated they've got the skill and the fortitude to solve the largest single negative problem that's facing us." Technically, the credit for reaching the settlement went to Lester W. Brann, president of the Illinois State Chamber of Commerce (ISCC) and Robert G. Gibson, president of the Illinois American Federation of Labor-Congress of Industrial Organizations (AFL-CIO). But Brann, Gibson and the rest of the business and labor leaders involved knew they couldn't have negotiated the agreement without the "help" of House Speaker Michael J. Madigan and Senate President Philip J. Rock, the leaders of the Democrat-controlled legislature, and Thompson, a Republican. "We have achieved the unachievable," Thompson went on to say at the news conference. ". . .I think we have set the pattern for leadership in the nation .... I think all of us can turn united efforts to Washington to obtain relief under federal law." The reform was orchestrated to persuade Congress to relax the two penalties the feds impose when state UI trust funds borrow from the federal UI trust fund. But the reform was also designed to return the state UI trust fund to solvency, repay some of what the state fund has already borrowed from the federal fund and reduce what the state fund will borrow in the future. Technically, the $2 billion agreement doesn't solve the state's UI problem since it doesn't eliminate the need for the state trust fund to borrow from the federal trust fund by the time the terms of the agreement expire in 1986. But the agreement at least puts the state fund in the position to repay some of what it has borrowed — as well as meet its own payout of benefits. Illinois wants Congress to defer the $50 million in interest that state government must pay in October, and to, cap the federal UI penalty tax on IIlinois business to produce $140 million instead of $225 million in calendar 1983. Thompson says the Illinois reform meets the standards Congress is expected to set for relaxing the penalties on the states. The pending federal legislation to relax the penalties is part of the Social Security bail-out bill, which in late March was in conference committee. Under the legislation no state would have its penalties relaxed unless its state UI trust fund comes closer to meeting its own payout of benefits in the next three years. The Illinois reform meets that test, Thompson said. The $2 billion agreement calls for "savings" just as the federal legislation requires each year: $300 million more in taxes and $240 million less in benefits in calendar 1984; $360 million more in taxes and $240 million less in benefits in 1985; and $500 million more in taxes and $300 million less in benefits in 1986. Having met this test, according to the pending federal legislation, Illinois state government would be required to pay only $10 million of the $50 million in interest due in October 1983, paying the remaining $40 million in installments in the next three years. The other advantage in meeting the test is a reduction in the federal UI penalty tax on Illinois business. Illinois business currently pays federal UI taxes at the rate of 1.4 percent of its taxable wage base; .6 percent of that is the penalty tax levied because the state UI trust fund has not repaid what it has borrowed from the federal UI trust fund. The federal UI penalty tax was set to go up to .9 percent in 1983. If the federal legislation passes, the penalty tax will rise to only .7 percent and stay at that level for the next three years. Illinois business is expected to pay $225 million in the federal UI penalty tax in 1983, but the federal legislation would hold it to $140 million this year and at $164 million in the next two years. The call for state UI reform this year came first from Thompson in his inaugural address January 10; Madigan echoed that call in his inaugural address as House speaker two days later, telling legislators that state UI reform was the major issue they faced in the May 1983 | Illinois Issues | 26 spring 1983 session. (Of course Madigan's remarks were made before Thompson called for a raise in the income tax and other state taxes in his State of the State address February 8.) Once business and labor sat down at the Executive Mansion bargaining table March 5, it took Brann and Gibson only two weeks to negotiate the $2 billion agreement.

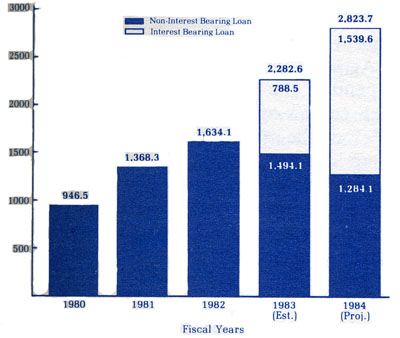

That was a replay of the scenario two years ago, except the timing was different. In 1981 Illinois business was paying $130 million a year in the federal UI penalty tax, and Congress was threatening to charge Illinois state government interest on what the state fund borrowed from the federal fund. Business and labor went to the Executive Mansion on June 16, 1981, and Brann and Gibson emerged with a $500 million settlement two days later, in which taxes went up $240 million and benefits went down $260 million. Brann and Gibson said then they had solved Illinois' UI problem. But in 1982 the feds started charging the state interest; in 1983 Congress removed a temporary cap on the federal UI penalty tax. And the recession went on. Under the 1983 reform, the state UI trust fund will show a balance by 1986. The fund had showed a deficit of $800 million in January 1983, and without the reform, the deficit was expected to peak at $975 million by 1984, dropping to $200 million by 1987. Because of the reform, the deficit is expected to drop to $739 million by 1984 and continue to drop until 1986, when the fund should show a balance of $90 million (the first balance since 1980). The balance should rise to $499 million by 1987, but the "surplus" will be used to pay the state debt to the feds. Despite the agreement, that debt will be formidable. By 1987, Illinois will still owe the feds $1,783 billion in UI loans. The federal UI trust fund had lent the state UI trust fund a total of $2,070 billion by calendar 1983; that included $1,629 billion borrowed before the feds began charging interest in April 1982 and $441 million borrowed since. Both loans must be retired via a combination of the state UI taxes on business and the federal UI penalty tax on business, but the interest-free loan must be retired before the interest-bearing one. If the legislation pending in Congress to cap the federal UI penalty tax in 1983 should fail, Illinois business will pay $780 million on the interest-free portion of the loan by calendar 1987. With a cap, business will pay $630 million by 1987, when the loan would be down to $999 million. Either way, Illinois would still be borrowing from the feds to fund projected UI benefits, and would be charged interest on all these loans. Illinois expects to borrow another $445 million by calendar 1987, when it would owe a total of $886 million. Without the reform, the loan was expected to reach $2,197 billion by 1987. The negotiation process centered on how business and labor would split the burden for state UI reform. Business agreed to $1,220 million more in taxes and labor to $780 million less in benefits; that amounts to a 3:2 split. Brann said that despite the heavier burden on business, he believed the reform leaves Illinois competitive with other midwestern industrial states. He said business bears a greater burden in UI reform in other Great Lakes states: 3:1 in Ohio, 4:1 in Michigan (and negotiations beginning at 5:1 in Wisconsin). The lighter UI burden on Illinois business is linked to the governor's tax increase proposal. Knowing business would have to agree to higher UI taxes, Thompson proposed a corporate income tax increase that would be less than the personal income tax increase. Under the reform, both the wage base at which business is taxed and the rate at which it is taxed went up. The wage base will rise in two steps, from the current $7,000 to $8,500, by January 1, 1985. The range of rates, currently .6 to 5.7 percent, will rise by a series of steps to .8 to 7.3 percent by January 1, 1986. Labor also met its goals according to Gibson: to maintain current standards for eligibility and qualifications and to maintain maximum benefits at $200 a week for persons with dependent children. Under the reform, maximum benefits fell April 24, and will stay low for about nine months, until February 1 when they will rise but not return to the current level. Benefits for persons with dependent children drop from $224 a week to $200, but will climb to $209; benefits for persons with a dependent spouse fall from $201 to $177, then rise to $184; benefits for single persons with no dependents drop from $168 a week to $154, then rise to $161. The "solution" to Illinois' UI problem is based on several assumptions, chiefly that unemployment will not exceed the projections. The reform assumes unemployment will run 10 percent in calendar 1983, fall to 9.4 percent in 1984 and stay at 8.5 percent in 1985 and 1986. Reform also assumes that Congress will, for the next three years, defer the interest that Illinois state government owes and cap the federal UI penalty taxes Illinois business owes. Whatever Congress does, the state reform will still go a long way to assure the state trust fund has the ability to meet its own payout of benefits. But if the General Assembly fails to pass some kind of package of tax hikes, where will Illinois get the money from its already squeezed general funds to pay the interest when the deferred payments come due in the years to come?□ May 1983 | Illinois Issues | 27 |

|

|