|

Home | Search | Browse | About IPO | Staff | Links |

|

Home | Search | Browse | About IPO | Staff | Links |

|

By JENNIFER HALPERIN

Pension deficit haunts future

State government is the biggest employer in Illinois; but the state is years behind in funding its pension system It's not unusual to see lawmakers toting their offspring around the state Capitol complex when the General Assembly is in session. Just about every kid enjoys seeing where his or her parents work. But Sen. Steven J. Rauschenberger (R-33, Elgin) had a point to make when he brought his 10-year-old son Michael to Springfield during the spring legislative session and introduced him around to some colleagues. At the time, the freshman senator was trying to help push through a plan that would have firmly set Illinois on the long road toward fully funding its five pension systems; the state now has promised nearly $13 billion more in future pension benefits than it has put in the bank including expected interest earnings to pay those benefits. The plan Rauschenberger advocated would have required the legislature to set aside millions of dollars annually for the next 47 years so that eventually the state's assets catch up with its obligations. "I took Michael around to meet people, and as I did I said, 'He's going to be 57 years old before the state finishes paying off the pension liabilities we've promised if we adopt this [47-year system]," Rauschenberger said.

This huge deficit for the state was built up for many reasons. Not only have current and past legislatures and governors failed to fund the pension systems as needed; they have approved pension "sweeteners" such as improved medical benefits and higher salaries that have driven up the state's unfunded liability, critics say. The Illinois Constitution guarantees current and promised future pensions will be paid; the pressing question is: Where will the money come from to do so? "We're talking about a tremendous amount of money money that my son's son is going to have to pay. What we're doing is very, very unfair," Rauschenberger said. Such admonishments have become familiar refrains around the Capitol. In part, they are due to national surveys that rank Illinois among those states with the largest pension funding gaps. But the issue also has reaped attention through vocal pleadings from some unlikely "partners." This meeting of the minds personifies the cliche that "politics make strange bedfellows." It demonstrates that harsh economic problems can unite even those with

July 1993/Illinois Issues/17 divergent philosophical views. For example, the cries of doom issued regularly by veteran Illinois politico, law professor and long-time pension funding critic Dawn Clark Netsch, the state's socially liberal female comptroller, have been taken up by a band of five male freshman Republican senators, which includes Fitzgerald, Rauschenberger, Chris Lauzen (R-21, Aurora), Patrick O'Malley (R-18, Palos Park) and Dave Syverson (R-34, Rockford). "Both parties are nervous about it," said Fitzgerald. "Anybody who cares about the long term at all is going to have a problem with it." As a state senator in 1989, Netsch sponsored what became Public Act 86-273, which called for a pension funding schedule with a 40-year amortization to be phased in during the subsequent seven years. "We would have been relatively home free on that schedule," Netsch said. But it never was funded. Similar to the way in which our federal government can't seem to abide by laws intended to force them to pass a balanced budget or have spending cut automatically, the Illinois legislature has found a way to circumvent its own law. This year, the Republican Senate pension package would have renewed PA 86-273's intentions and set in place a funding mechanism. But without a funding source, it didn't have much of a chance. Instead, lawmakers passed a resolution forming a task force to study long-term planning for pensions sytems, including funding practices and benefit levels. As bad as the situation is and has been for years for state pensions, public officials have engaged in some unabashedly risky game-playing with pension funds, critics charge. "These games have been going on a long, long time," said Fitzgerald. "I can tell you the previous [gubernatorial] administration started the big games, but they've been going on for ages and ages."

The "five plus five" issue struck Rauschenberger as particularly frustrating. "It didn't appear as though much weight or thought or analysis went into the costs of this plan. When we set the stage for wonderful early retirement, other groups [of public employees] want them," Rauschenberger said. "It's like a ripple effect. As soon as one group gets one leg up, the others want to level the playing field. "We've already forced these problems onto the next two generations if you define a generation by 30 years," he added. "We're finally focusing this year on it, but up until now we've been totally out of line with what the rest of the world does. General Motors, Caterpillar they all see that pension sweeteners [such as continued medical insurance coverage with no retiree contribution] may end the company. If we were a private company, our attorneys may counsel dissolution of the company and coming to a settlement with retirees." As employees take advantage of early retirement plans like "five plus five," the state must pay them for accumulated unused sick days and vacation. State workers can amass up to 12 sick days a year for their entire career. When they quit or are fired, the state pays them for half of the unused

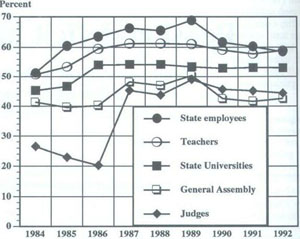

18/July 1993/Illinois Issues days and adds the other half of that cash value to their pensions. And unused vacation days can be cashed in when they leave. So, for example, when 46-year-old Ronald H. Grimming, deputy director of the Illinois State Police, took advantage of "five plus five" to leave his $73,000-a-year post earlier this year, he collected a lump sum of $33,030.56, according to the comptroller's office. What's more, he then took a $77,250-a-year job with the Florida Highway Patrol. "When we were playing games in the '80s, the stock market was so up it almost made up for underfunding," said Fitzgerald in reference to high interest yields the pension systems were getting from their investments. One habit consistently pointed out as devastating to the pension funds began in 1982, when the state stopped contributing enough money to the funds to cover checks going out in the same year. The stock market was doing well, so pension funds' investment income was up. In response, former Gov. James R. Thompson reduced state contributions to less than two-thirds of the 1982 payout to retirees. That practice was supposed to be limited to one year but was not. "I've made the observation that if the state had been able or willing to fund the pensions more expansively in the early '80s, our asset-to-liability ratio would have been much bigger now," said James D. Nowlan, president of the Taxpayers' Federation of Illinois. "The state did not take advantage of that but of course that's hindsight." Investments are decided by the retirement systems' boards of trustees, whose members are named in a variety of ways. Some are appointed by the governor, some represent other top state officials such as the comptroller's office or the governor's Bureau of the Budget, and others represent system members. "I've never heard it said or even suggested that the investments are not good," said Netsch. "That's what sustained us a lot of those years because the returns were so high." Fitzgerald agreed. "The problem is not the boards, whose responsibility is to invest. The problem is the legislators' and governor's propensity to not say 'no' to pension sweeteners." When the high investment returns of the '80s dropped, the state retirement systems were left without the cushion those returns had provided. Further aggravating the situation is the sweetening of pension deals for future retirees without money set aside to pay for them. Some examples were outlined in the state's Comprehensive Annual Financial Report for 1991. During that fiscal year, lawmakers increased pension benefit obligations for the State Employees' Retirement System (SERS), which covers most state employees not eligible for another state-sponsored plan. They added 3 percent annual increases for disability benefits and accidental death annuities. That year lawmakers also hiked the obligation for the State Universities' Retirement System (SURS), approving a new 3 percent post-retirement benefit. Moreover, the state has picked up portions of employee contributions to pension plans when it can not afford to give raises but without setting aside the additional money to pay those contributions. For example, until January 1, 1992, most state employees contributed 4 percent of their pay toward their pensions. But after that date, the state began making the contributions in lieu of raises. "Now virtually the entire onus for funding the State Employees' Retirement System is placed on the state budget," states the fiscal year 1994 report on pension funding requirements prepared by the Illinois Economic and Fiscal Commission. "Why would we rather pick up the 4 percent contribution for state workers?" Fitzgerald said. "Because it costs us nothing. In essence we're just borrowing from the future." The fact that Illinois is nearly $13 billion behind in pension funding means this: If the state was to shut down, the money it has set aside for all retirement benefits would pay only 57.1 percent or 57.1 cents for every dollar owed even figuring in the interest that would have accrued on the state's pension investments. "There is some disagreement of an essential level of funding for pensions," said Netsch. "But no one believes 57 percent is even close to adequate. Eighty-five percent is considered probably secure enough. But people wouldn't dream of 57 percent." "Actually, a system is healthy if it is fully funded 100 percent," said Ronald D. Picur, former comptroller of the city of Chicago and now associate professor at the University of Illinois at Chicago, where he is acting head of the accounting department. "Obviously, the farther you get away from [a fully-funded system], the more you're pushing off onto the future." Picur said the best way to assess Illinois' standing is to look at the state's individual pension systems and the percentage of which each has been funded over several years. For instance, SERS was funded at 69 percent in fiscal year 1989 and 59 percent in fiscal year 1992, according to the Illinois Economic and Fiscal Commission. Similarly, the other four systems saw their funding percentages drop during the same time period. Those systems include: the Teachers' Retirement System (TRS), covering teachers employed by public school districts in Illinois except those in Chicago; SURS, covering faculty and staff of state universities, community colleges and related higher education agencies; the Judges' Retirement System (JRS), covering judges and associate judges of the Illinois courts; and the General Assembly Retirement System (GARS), covering members of the General Assembly and certain state officials, including the governor. "Uniformly and consistently, the trend is moving in the wrong direction," said Picur. "That, to my mind, is a warning signal; it's a red flag." Even the federal Social Security system, which is the subject of its own share of hand-wringing, is funded in a more actuarially sound way, he said. But everyone from Picur to Netsch to the state's auditor general's office is quick to point out that despite these ominous numbers, every state employee is going to get every penny they're owed. Currently, more than 98,000 people are receiving benefits from the five retirement systems. "We're all going to get our pension benefits," Netsch

July 1993/Illinois Issues/19 assured, explaining that they are guaranteed by the state Constitution. What's more, a "non-diminishment clause" forbids lawmakers from lessening the benefits. "We're constitutionally precluded from changing it," said Rauschenberger. "We can't undo others' good intentions. We've made a lot of policy decisions we're going to come to regret." And it's unlikely a constitutional amendment changing these policies would get much support, he said, because of a "terribly involved constituency" of former and current state employees. On the contrary, he said, these constituents are constantly putting pressure on legislators to sweeten benefits. "When we address pension issues, there are a quarter of a million [future] beneficiaries we're talking about." Netsch agreed: "We're talking about the retirement rights of hundreds of thousands of people. They made a deal with their employers, and the state has at least made an implied promise that they'd be funded." Some factors affect the state's pension obligation no matter what state officials do, such as a change in predictions of how long retirees are expected to live and thus collect benefits. For example, at TRS, a change in post-retirement mortality actuarial assumptions in fiscal year 1991 increased the pension benefit obligation by $214,173, according to the state's Comprehensive Annual Report from that year. But are things on their way to getting any better in the areas that legislators can control? "There have been several bills killed in both the House and Senate this year that would've sweetened pensions for state employees," said Fitzgerald. "In part I think that's because of the revived focus on pension problems. Every year for years there have been big, sweet pension sweeteners. Nobody really lobbies against that stuff because the cost isn't apparent right away." "There's been no formal pledge to keep all pension sweeteners out," said Mark Gordon, spokesman for Senate President James "Pate" Philip (R-23, Wood Dale). "Early in the session Pate was trying to work with the speaker toward a pledge to put a freeze on pension changes, but it never got done. It wasn't the speaker's fault; it just never happened. This is a recognition that there's no money for this." Steve Brown, spokesman for House Speaker Michael J. Madigan (D-22, Chicago), agreed. Philip and Madigan cosponsored the resolution creating the pension task force this session. "This isn't just a lot of talk because we talked to Pate and the governor's office, and they're frankly pretty nervous," said Fitzgerald. But nervousness doesn't provide money where there is none, he acknowledges. "I think in some sense having a continuing [source of money that would go toward filling pension obligation] is a good idea, but we'll have to have a funding source for it," he said. Fitzgerald said it would be wise for the new pension task force to play a "legislative watchdog" role, analyzing the full future effect of bills calling for pension sweeteners, early retirement offers and general funding for the systems. Establishment of an income tax on pension benefits has been mentioned as one possible solution to the mounting pension debt. "Almost every state with an income tax imposes the tax on pension income, which Illinois doesn't," said Ron Snell, who analyzes pension issues for the Denver-based National Conference on State Legislatures. "What you're doing is not real common." "Most pensioneers don't realize they're not paying income tax on them," Fitzgerald said. "[Such a tax] could net $150 million a year depending on how widely it was applied." California is so squeezed for revenue that it is trying to impose its state income tax on state pension benefits paid to retirees now living outside of California. The rationale in pursuing that tax is that contributions to state pension plans were not subjected to the tax, so the state now should be allowed to collect income tax on benefits. Other suggestions include offering lower benefits for new employees, which would amount to a "two-tier system," or hiking employee contributions to the plan from current levels. And some advocate changing to what's known as a defined contribution plan instead of the defined benefit plan now in place. In defined contribution plans, known as 401k's, an employee can choose to put a small portion of his paycheck into a retirement account. The employer may make periodic matching contributions, but the employee decides how to invest the money. Under a defined benefit plan, the employer promises to pay a certain amount to retired employees each month based on such factors as length of service and salary at the time of retirement. The spring 1993 legislative session turned out not to be the time for dramatic action on funding pension obligations. But is such action truly on its way in the near future? "If we don't do anything soon, years down the line it could mean several more points of income tax dedicated just to pension funds," Fitzgerald said. But like the looming federal deficits that continues to hang over the country, the pension issue lacks immediate consequences which usually are needed to spur elected officials into action. "It's easy to see why this appeals to budget-writers," said Marjorie Shea, legislative chair of the Illinois Retired Teachers Association. "The politicians now in office will be off collecting their own retirement benefits by the time this problem surfaces." "It's not the kind of thing that stands up and bites a politician where they ought to be bitten," Netsch said. "It is a chicken that is going to come home to roost, or you can use any other metaphor you want to make up." Rauschenberger agreed. "I had high hopes in the beginning of this year that we'd begin to address this," he said. "Next year it will be harder because we'll be that much closer to major elections." Of course, relatively minimal service is required of lawmakers for pension eligibility. Even if a legislator is unvoluntarily "retired early" by not winning reelection, he or she needs to have served just four years to be eligible for pension benefits at age 62. For eight years of legislative service, retirement age is 55 with full benefits.

20/July 1993/Illinois Issues |

||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|