|

Home | Search | Browse | About IPO | Staff | Links |

|

Home | Search | Browse | About IPO | Staff | Links |

|

Fiscal Program Evaluation

by RICHARD MANSELL

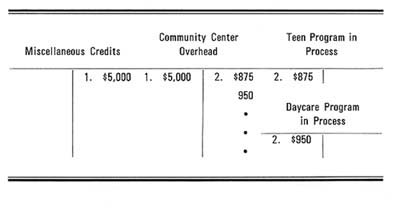

Each program or service offered by a Park and Recreation agency has both direct and indirect costs. The direct costs are usually direct labor and direct material (e.g., for an art class these would be the instructor's wages and the appropriate art materials). The indirect costs, which can also be referred to as program overhead, include a much wider range of costs. Some of these costs might be: Indirect labor: Janitorial, clerical, maintenance wages, etc. Repair costs. Light, electricity and head coats. Supplies: paper, small tools, cleaning supplies, etc. Administration: phone, car allowance, office supplies, etc. Taxes: property and payroll. Insurance. Depreciation. Advertising: brochure, newspaper, radio, etc. (Some of these indirect costs might be treated as direct costs thus cutting your indirect cost allocations.) The recording of these expenses is necessary if the people responsible for the different programs are expected to prepare budgets which reflect the true situation. If we are to talk of programs which break even, make a profit or loss, then all relative costs must be included in determining the Summary Income statement. If full costs are not accumulated for the appropriate program then some other program or department will have to absorb these costs. Also for control and improvement purposes, budgets based on these criteria can give us a realistic picture of what is really occuring. There is a three step process in the accounting procedure before the cost is actually applied to the specific program. First, the overhead costs must be recorded by the overhead (responsibility) centers within the department. This is called distributing the cost. Thus, labor costs for maintenance for the month might be distributed to each of the following departments: administration (main office), swimming pool, community center, senior citizen center, etc. The time each laborer spent at each place would be calculated and the costs distributed appropriately. The next step is to assign (this is called allocating the costs) all overhead costs to the appropriate operating departments. The reason for this is to differentiate between service and operating departments (an operating department being one which directly offers programs to the public and a service department being one which offers services to the operating departments). The administration center (service department) costs need to be allocated to the operating departments. This allocation is often done by using some arbitrary bases, or may be done by assigning overhead rates of which more will be explained later. Once the costs have been allocated it is time to absorb or apply the overhead cost to the program. This absorption of costs allows the indirect costs to be assigned to the specific programs. Methods of absorbing overhead will also be explained shortly. Let's first look at an example of how this process would work. The community center of Good-life Parks and Recreation Department has incurred $5,000 of indirect costs during the month of March (1. Record the incur-rence of the actual overhead costs). $875 of the overhead (determined through the use of overhead rates) is applied to the teen program and another $950 applied to the daycare program, etc. (2. Record the absorption of overhead to program).

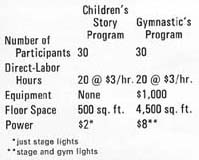

Illinois Parks and Recreation July/August, 1975 This method will often leave a balance in the overhead account. This balance may be either closed out at the end of each month or at the end of the year. This balance may be viewed as a gain or loss and closed into a variance account which is then closed into the Income Summary. It can also be viewed as an adjustment to the cost of the program and thus assumes that the original overhead rate estimates were incorrect and appropriate corrections should be made. It is probably easier to close the balance into the variance account but if there is a consistent overhead balance occuring each month then adjustments to the overhead rates will have to be made. To be able to compute the cost of a program more exactly it is necessary to assign overhead costs to the centers where they are incurred. It is not always possible to do this with 100% accuracy but various methods can be used in an attempt to be as close and fair as possible. Generally a system of overhead rates is established. Usually the allocation of overhead costs to the operating departments is based upon the benefits actually received by that department. Thus, if the maintenance man spends eight hours repairing the floor at the senior citizen center then that center is billed accordingly. It is not always quite so simple, and at times it is not known exactly how much of the overhead cost should be applied where. This is certainly the case when attempting to determine the application of overhead costs to the specific program. For example, let's consider two community center programs:

Assuming that the following costs are budgeted for the year:

Depreciation of Equipment........ $100

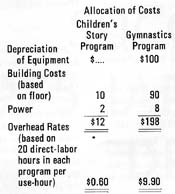

Direct costs per participant would be $2.00 (based on number of participants and costs of direct labor). If only one overhead rate based on direct-labor hours was used then each program would have an overhead rate of $5.25 per use-hour or $3.50 per participant per program. Then it would cost $5.50 ($2.00 direct plus $3.50 indirect costs) to supply the program for each individual attending either the storytelling program or the gymnastics program. It is seen that by using only one overhead rate the program costs are not fairly allocated. The alternative is to compute overhead rates for each program.

The cost of the storytelling program per participant will be $2.40 (direct cost of $2.00 and $0.40 indirect costs per participant) . The cost of the gymnastic program per participant will be $8.60. There exists no standard rules for the basis of allocating overhead costs to the various programs.

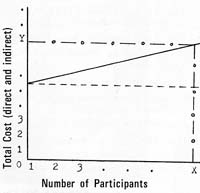

Once a fair system of determining and allocating costs has been established it enables a simple process of determining fee structure to be implemented. Program Cost Model The cost per participant for the program ($A) is determined by dividing the total cost ($Y) by the number of participants (X). Deciding on whether the program should operate on a break-even basis or otherwise is another matter and entails consideration of a number of other factors. This method of recording costs will enable the administrator to assign costs where reasonably applicable. This is important for determining costs of programs and for the control of such costs. This does not imply that a program will be cancelled if full costs cannot be recovered as this decision may well take into consideration other pertinent factors. However, the availability of accurate fiscal information will improve the quality of these final decisions. (Richard Mansell, native of British Columbia, Canada, is presently a Ph.D. candidate in the Department of Recreation and Park Administration at the University of Illinois, Champaign-Urbana.) Illinois Parks and Recreation July/August, 1975 |

|

|