|

Home | Search | Browse | About IPO | Staff | Links |

|

Home | Search | Browse | About IPO | Staff | Links |

|

Why Should I Refund My Low Coupon Bonds?

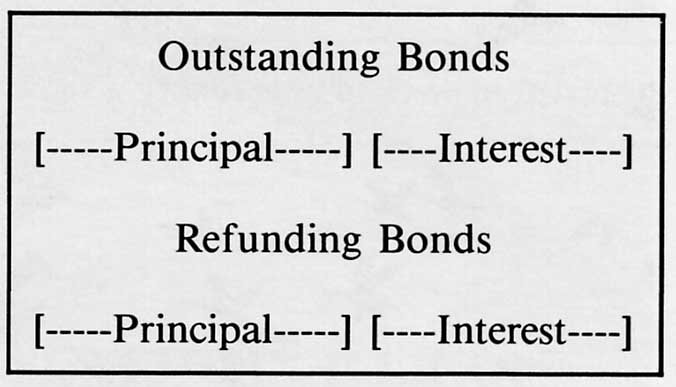

Question: Why are some Illinois park districts swapping in their old 5% bonds for new debt with significantly higher coupons? Answer: For the Money! In this article, the author details the advantages of a "low-to-high" refunding and explains how you can decide if refunding is right for you. By Stephen R. Willson Introduction: If you sold bonds in 1981 or 1982 when interest rates were very high, the purpose of refunding is clear: you can save money by substituting low coupon bonds for high coupon bonds. But several Illinois park districts have recently done exactly the opposite: refunded older bonds that bear very low rates of interest. Why would anyone do that? This article explains why without complex mathematics, so you can decide if refunding is right for your district. Why Refund? The biggest reason park districts, and other non-home rule governments are refunding old debt is to free Corporate Personal Property Replacement Tax (CPPRT) revenues for operating purposes. By refunding bonds issued prior to January 1, 1980, CPPRT is freed from the first lien, debt service, and can be transferred to the operating fund. This is called a "low-to-high" refunding (low coupons to high coupons) and, despite the higher interest rates, debt service need not increase. The second reason to consider a "low-to-high" refunding is to restructure debt service. It is important to note there are no federal regulations regarding the maturity structure of refunding bonds; the new bonds can be shorter or longer than the debt they replace, increasing bonding capacity or reducing annual tax levies for debt service. Advance Refunding: An Explanation: Officials interested in refunding their bonds need to understand how refunding works in order to make an informed decision. Refunding can best be explained by comparing it to something familiar: refinancing a mortgage. When a mortgage is refinanced, the old mortgage is immediately paid off and a new mortgage takes its place. Refunding municipal bonds is not identical to refinancing a mortgage because bonds normally can't be paid off immediately. Instead, when refunding bonds are sold the proceeds are used to purchase U.S. government securities which are deposited into an escrow account. The cash flow from this escrow account pays the debt service on the old bonds. The old bonds are "defeased" — that is, the issuer is no longer liable for them. If you currently have cash in your debt service fund, you can either put it in the escrow account, or use it to pay debt service on the new bonds. You may not legally transfer this money to your operating fund. There is one important fact to note: the yield on the escrow account is not permitted to exceed the yield on the refunding bonds. Characteristics of a Low-To-High Refunding: The first surprising characteristic of a "low-to-high" refunding is that the par amount of the new debt will be less than the par amount of the old debt. The decrease in the par amount of debt outstanding almost exactly offsets the increase in interest. This is shown graphically below:

This means "low-to-high" refundings are not sensitive to interest rates. Basically, as the interest rate rises, the par amount of the bonds falls, and there is no net effect on total debt service. Thus, as a park district official you needn't consider the level of interest rates in deciding whether or not to refund. Finally, refunding bonds are not subject to referendum because they replace existing debt. Thus, refunding pre-1980 debt will result in a lower par amount of debt, the same debt service as before, and allow Corporate Personal Property Replacement Tax revenues to be retained in the Corporate Fund. To park districts levying at their limit, these additional revenues for operating purposes are usually very welcome. The Inherent Difference: Because of the relation between interest rates and the size of the refunding bond issue, structuring a refunding issue is inherently more difficult than structuring capital projects bonds. When capital projects bonds are sold, a maturity structure is established, and the bonds are brought to market. If the actual interest rate on the bonds differs from what was expected, this doesn't affect the par amount of bonds issued. However, the par amount of refunding bonds is directly related to interest rates. Thus, a maturity schedule cannot be properly structured without knowing at what rates the bonds will sell. If actual interest rates are higher than expected, the issuer will have sold too many bonds, and may violate (Continued on p. 40) ABOUT THE AUTHOR: Mr. Willson, an Assistant Vice President in the Public Finance Division of the First National Bank in Chicago, has specialized in refunding and other arbitrage bonds for five years. He has a Bachelors degree in mathematics and a Masters degree in finance. Illinois Parks and Recreation 27 March/April 1984 LOW COUPON BONDS (Cont. from p. 27) IRS regulations regarding over-issuance. If actual interest rates are lower than expected, an even greater problem occurs — the issuer may not have sold enough bonds to refund the outstanding bonds. In the worst cases, the district may be forced to withdraw the bond issue, damaging its reputation in the market. Finally, structuring a refunding issue requires detailed knowledge of federal arbitrage regulations and the bond market, as well as access to computer programs that can solve the mathematical problems. Few park districts find it economic to keep people with such expertise on their staffs. The solution to this dilemma is to negotiate the sale of the refunding bonds with an underwriter. Negotiating the sale gives the issuer the flexibility to structure the bond issue to meet the requirements of the marketplace. Selecting the right underwriter is very important. The underwriter should have a thorough knowledge of the mathematics required to balance the new issue to the outstanding issue, an up-to-date knowledge of federal regulations, plus the ability to successfully market the bonds. The underwriter must accurately assess bond market conditions to properly time the issuance of the refunding bonds so that the district can fully realize the anticipated benefits of the refunding. Illinois Parks and Recreation 40 March/April 1984 |

|

|